Roth vs. Traditional IRA, Which is Right For You?

Estimate your Roth IRA savings by entering your age, contributions, and expected returns. Compare Roth vs Traditional IRAs to plan for a secure ret...

Written by

Alicija Dearth, CFP®

Planning for retirement can be complex, but tools like an Roth IRA calculator make it simpler to pick the ideal retirement savings method for your situation. An IRA calculator allows you to compare how using a Traditional IRA vs. Roth IRA can impact your future retirement account balance and potential tax savings. Whether you're considering opening an IRA or you've been contributing for years, this tool will help you understand which retirement method can help maximize your future wealth.

What's your desired retirement age?

65

Your estimate IRA balance

$253,231

Potential tax savings with Roth IRA

$96,883

Roth IRA vs Traditional IRA

Account balance as you age

This calculator estimates the amount of assets at retirement age using assuming a constant rate of return while adjusting the annual contributions based on inflation. At the retirement age, it assumes a constant withdrawal percentage for each year of retirement through age 85. It further assumes that accumulation in a taxable account will require a 25% higher withdrawal each year to satisfy a 20% income tax.

An IRA calculator is designed to help you project the future value of your account and potential tax savings available with a Traditional vs. Roth IRA, based on factors such as:

1. Contributions

3. Withdrawals

1. Gather Necessary Information

Before using the calculator, have the following details handy:

2. Input the Data

Most calculators allow you to enter:

3. Review the Results

Once you've entered your data, the Roth IRA calculator will display:

To show how an Roth IRA calculator works, let’s look at a few scenarios:

Example 1: Starting Early

With this scenario, your IRA could grow to $2.5 million by the age of 65. By using a Roth IRA, you could potentially save $770k when taking distributions during retirement.

Example 2: Starting Later

If you start at 40, your IRA could grow to $703k by the age of 65. By using a Roth IRA, you could potentially save $215k when taking distributions during retirement.

Example 3: High vs. Low Return Rates

At a 5% return, the balance at age 65 would be around $678,00 with a IRA. You could save $207,000 during your retirement years by using a Roth IRA.

At a 8% return, the balance at age 65 would be around $1.3 million with a IRA. You could save $398,000 during your retirement years by using a Roth IRA.

How is the Roth IRA potential tax savings calculated?

This calculator estimates the amount of assets at retirement age using a constant rate of return while adjusting the annual contributions based on inflation. At the retirement age, it assumes a constant withdrawal percentage for each year of retirement through age 85. It further assumes that accumulation in a Traditional IRA will require a 25% higher withdrawal each year to satisfy a 20% income tax.

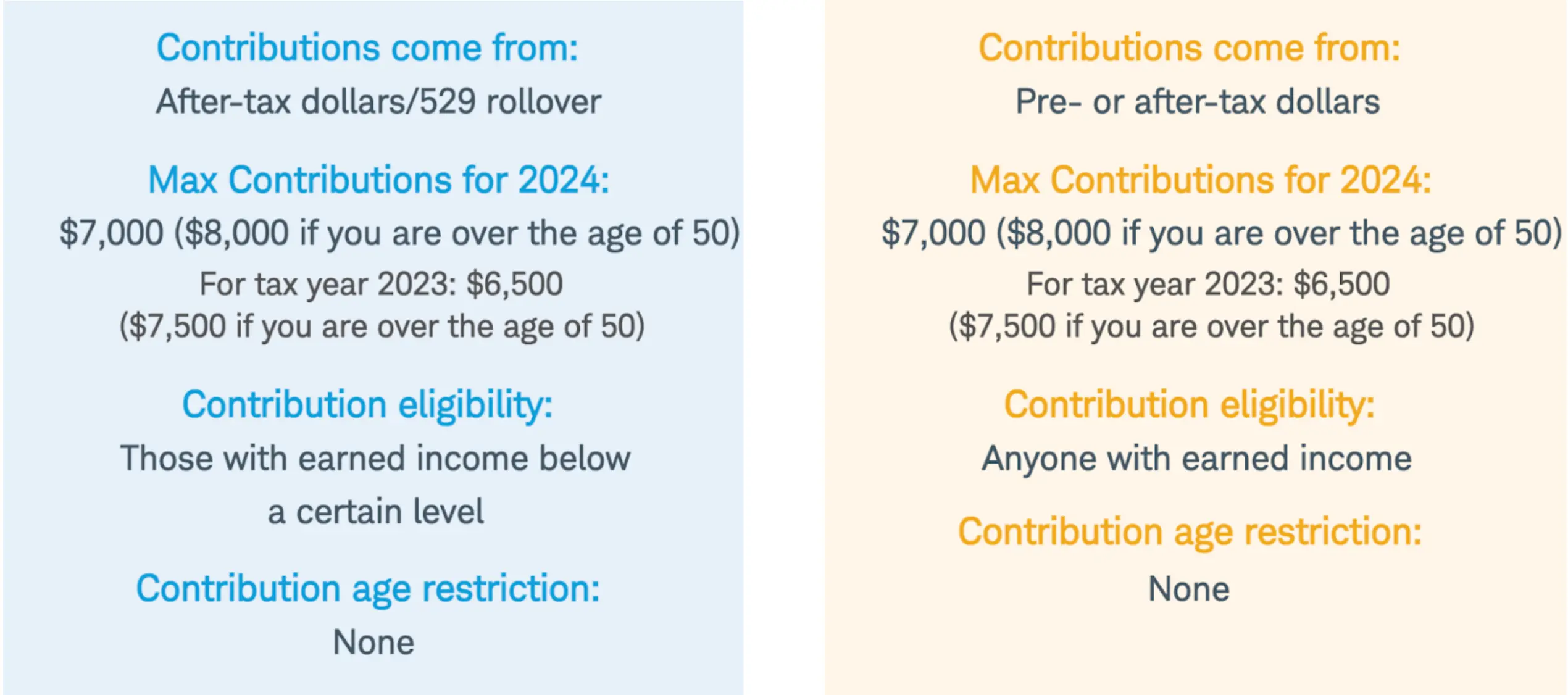

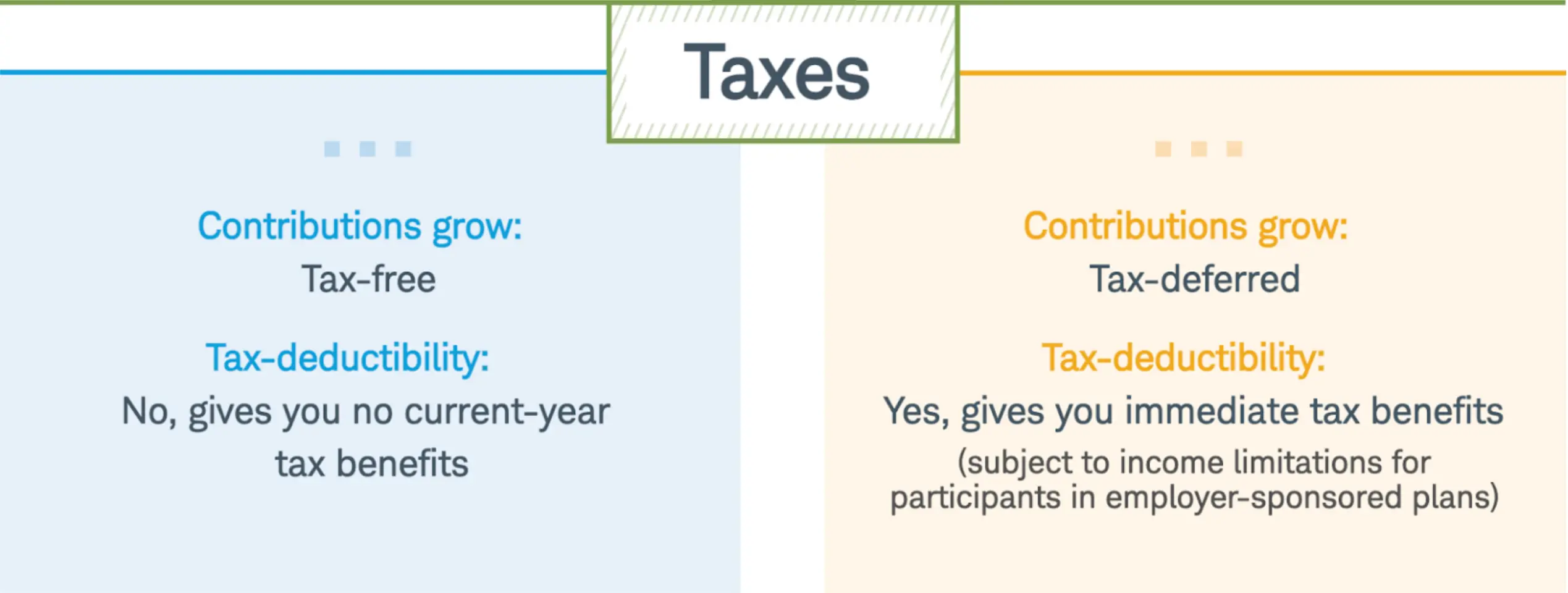

Who is a Traditional IRA best suited for?

An individual who expects to be in the same or lower tax bracket when starting to take withdrawals.

Who is a Roth IRA best suited for?

An individual who expects to be in a higher tax bracket when starting to take withdrawals.

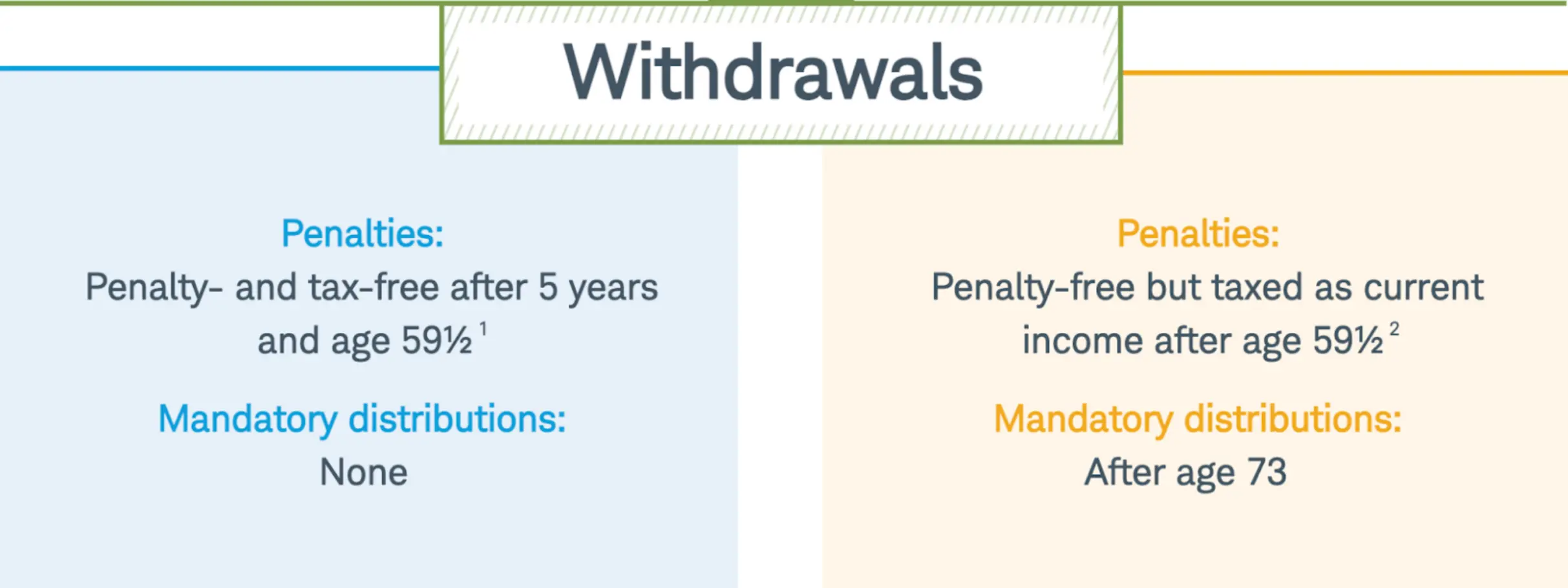

What happens after five years in a Roth IRA?

You can withdraw your contributions at any time, for any reason, without taxes or penalties. However, if you want to withdraw earnings tax-and-penalty free, the withdrawal must meet two conditions:

If you don’t meet both of these requirements, the earnings are subject to both income tax and a 10% early withdrawal penalty.